Climate Reporting Has Become a Finance-Grade Data Problem

Most organisations still think AASB S2 is about disclosure.

It isn’t.

The real challenge is whether organisations can defend the numbers behind the disclosure when investors, auditors, financiers, and boards begin asking harder questions.

Because climate reporting is no longer operating separately from financial decision-making.

It is rapidly becoming part of it.

A Climate Target Is Not the Same as a Climate Strategy

Across the market, organisations have announced net zero commitments, sustainability ambitions, and transition targets.

But targets alone are no longer enough.

Expectations are shifting toward evidence-based transition planning supported by operational data, financial assumptions, governance oversight, and measurable delivery pathways.

The organisations under pressure are not necessarily the ones without commitments.

They are often the ones without the infrastructure required to support those commitments.

That shift is already becoming visible through evolving disclosure expectations under AASB S2, increasing assurance scrutiny, and growing investor focus on climate-related financial risk.

The Market Has Moved Beyond Narrative Reporting

For years, sustainability reporting largely sat within communications, ESG, or stakeholder engagement functions.

That environment is changing quickly.

Climate disclosures are increasingly moving into finance, risk, governance, and audit functions.

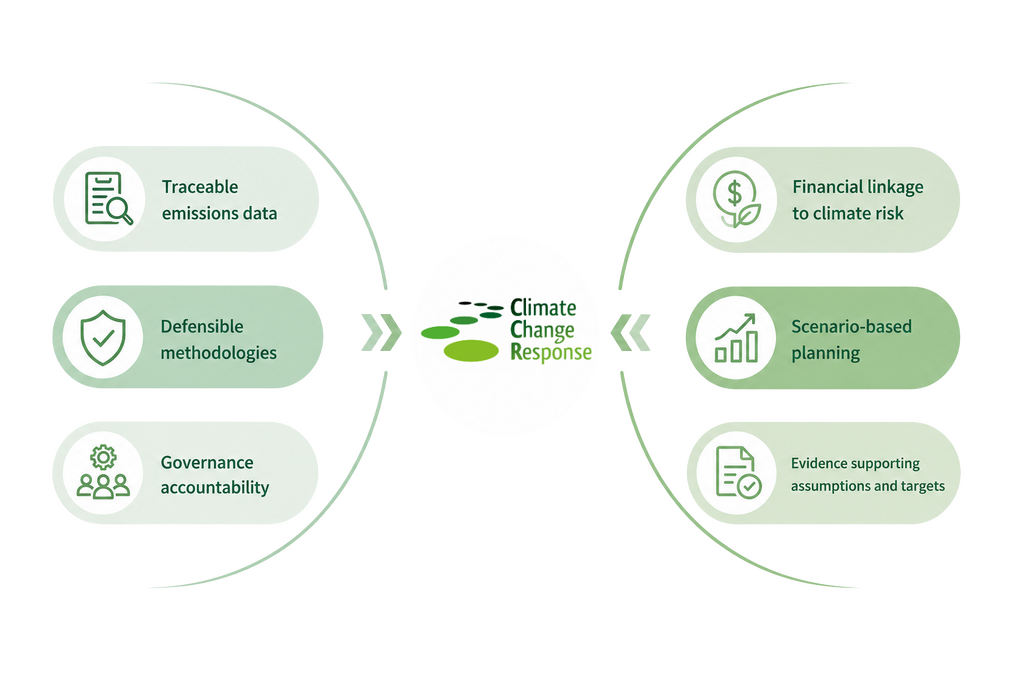

Organisations are now expected to demonstrate:

This is where many organisations are discovering the real challenge.

The reporting issue is not the PDF.

It is the fragmented data environment underneath it.

Across the Australian market, CCR is seeing organisations struggle less with disclosure formatting and more with fragmented operational data, inconsistent methodologies, disconnected systems, and limited audit traceability across Scope 1 to 3 reporting environments.

In many cases, the challenge is not the reporting framework itself. It is whether organisations have the systems, governance structures, and reporting workflows required to produce consistent and defensible climate information at scale.

Scope 3 Is Exposing the Infrastructure Gap

Most organisations can eventually work through Scope 1 and Scope 2 reporting.

Scope 3 is where operational complexity escalates.

In many organisations, this information sits across disconnected teams, systems, spreadsheets, and suppliers, often without consistent governance or audit traceability.

Yet these emissions categories frequently represent the largest share of total organisational emissions.

The GHG Protocol estimates Scope 3 commonly represents the majority of an organisation’s emissions footprint, while McKinsey analysis suggests value-chain emissions can account for approximately 90% of total emissions in some sectors.

The emissions most material to investors are often the ones organisations control least directly.

This Is Following the Same Pattern as Previous Reporting Transitions

Australian businesses have seen this before.

When IFRS reporting requirements commenced in Australia in 2005, many organisations underestimated the scale of system and process changes required beneath the reporting obligation.

A similar pattern emerged during the rollout of AASB 16 lease accounting requirements, which became effective from 2019 reporting periods.

The organisations that delayed preparation often spent significantly more later, not because the standards were impossible, but because the supporting infrastructure was not ready when scrutiny intensified.

Climate reporting is now entering the same phase.

Except this time, the data challenge is materially larger.

Financial reporting generally relies on structured internal financial systems.

Climate reporting requires organisations to consolidate operational, environmental, supplier, asset, and value-chain information from across the business ecosystem.

That is a fundamentally different level of complexity.

The Assurance Conversation Has Already Started

One of the biggest misconceptions in the market is that assurance remains a future problem.

It doesn’t.

The transition toward increasingly rigorous sustainability assurance expectations is already underway through evolving Australian and international assurance frameworks, including standards being developed and applied by the AUASB.

The gap between reporting and assurance-ready reporting is substantial.

Spreadsheets may support early disclosure exercises.

They rarely support scalable governance, audit traceability, version control, repeatable methodologies, or long-term assurance maturity.

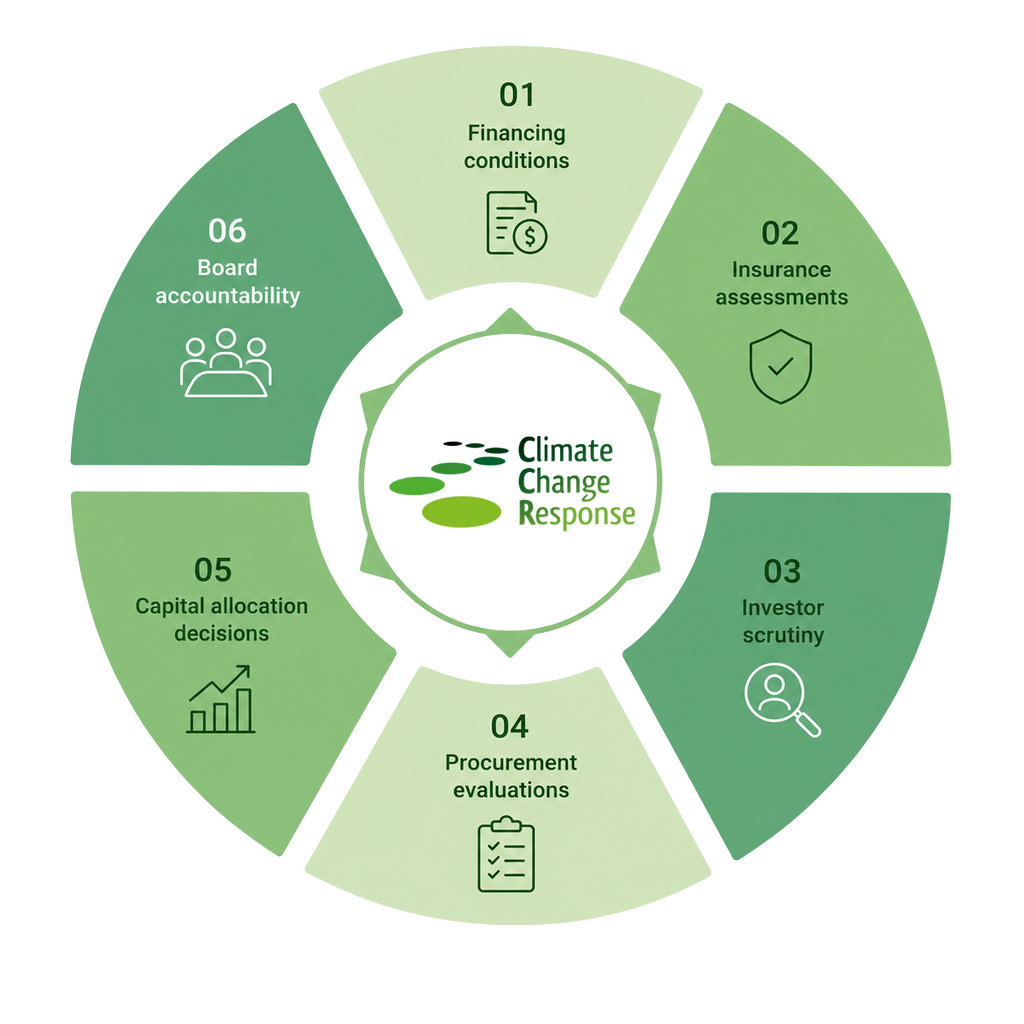

That becomes particularly important when disclosures begin influencing:

The commercial market is moving faster than regulation alone.

The Organisations Getting Ahead Are Building Capability, Not Just Reports

The strongest organisations are not treating climate reporting as a once-a-year compliance activity.

They are building operational capability around it.

This is increasingly driving investment into integrated sustainability data environments, automated reporting workflows, emissions management platforms, and governance systems capable of supporting audit-ready disclosures.

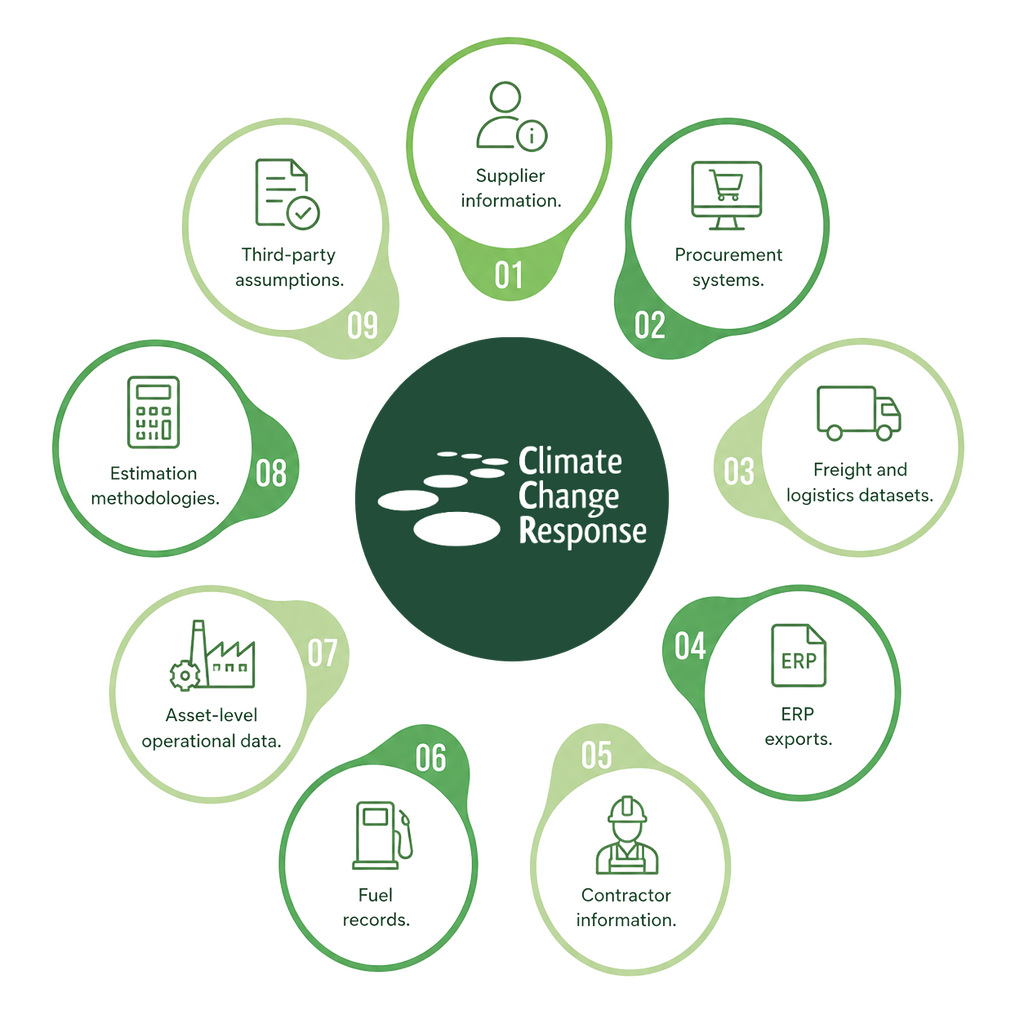

CCR is seeing growing demand for systems that can consolidate operational, environmental, supplier, and asset-level data into structured reporting environments aligned with evolving assurance expectations.

That includes:

Credible climate reporting increasingly depends on whether organisations can connect sustainability ambition to operational and financial evidence.

Not simply disclose targets.

The Real Shift Happening Under AASB S2

AASB S2 is not simply introducing another reporting framework.

It is accelerating a broader shift in how climate risk is assessed across the market.

Climate information is increasingly being evaluated with expectations traditionally applied to financial information:

Organisations still relying on fragmented manual processes may find the challenge is no longer compliance alone.

It is credibility.

The Bottom Line

The organisations that move early to strengthen governance, data infrastructure, and reporting maturity are likely to reduce long-term compliance risk and extract greater strategic value from the process.

The organisations that delay may ultimately spend the same investment later, but through remediation, reactive implementation, and accelerated assurance pressure.

Climate reporting is no longer just a sustainability exercise.

It is becoming a finance-grade operational capability.

Assess Your Readiness

CCR – Climate Change Response supports organisations across climate disclosure readiness, emissions data management, Scope 1 to 3 reporting, assurance preparedness, transition planning, and sustainability reporting transformation.

Through CCR’s advisory capability and integrated sustainability intelligence platforms, organisations can strengthen reporting governance, improve data traceability, and transition toward scalable assurance-ready climate disclosure environments.